What's next for cryptocurrencies?

Since Bitcoin’s launch in 2009, cryptocurrencies have spread across the economy. Viewed by some as high-risk assets and by others as a potential monetary revolution, their reputation now hangs in the balance.

Investigation by Nicolas Sandanassamy - Published on

Reality check for cryptocurrencies

Since Bitcoin’s launch in 2009, cryptocurrencies have moved beyond a geeky experiment or technological novelty. They are now part of the global financial system, with 17,000–19,000 in circulation, even if only a fraction is actively traded.

The impact is evident in public policies, economies and research, with El Salvador providing a striking example. After becoming the first country to adopt Bitcoin as legal tender in 2021, it made its use optional in February 2025. This partial retreat acknowledges what many have since recognised: widespread adoption of crypto-assets for everyday transactions has yet to materialise. This does not mean the experiment has failed. Around the world, the use of cryptocurrency persists, primarily driven by saving, speculative trading, technology and digital innovation.

The policy environment has also shifted. Since 2025, the United States under President Donald Trump has lifted probes into leading crypto companies, loosened sector regulations, established a national crypto reserve and pledged to make the country the world’s “crypto capital”. And the market has taken notice: transaction volumes have surged, institutional players have shown renewed interest and public debate has turned towards regulated use. These developments are creating a fertile field of study for economists, computer scientists and sociologists. Cryptocurrencies are, in effect, creating a “laboratory economy”: a global testbed for radical new ways of trading, accounting and governance.

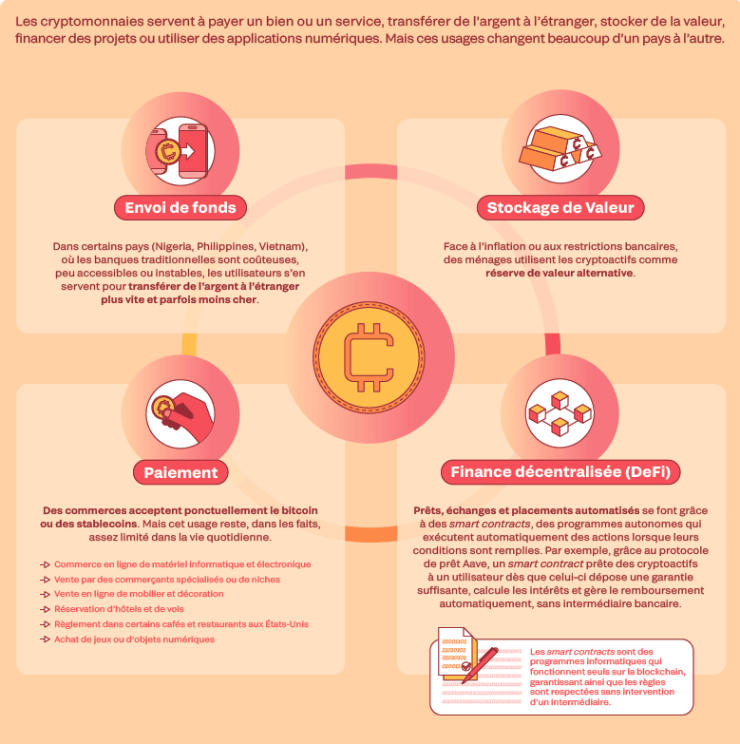

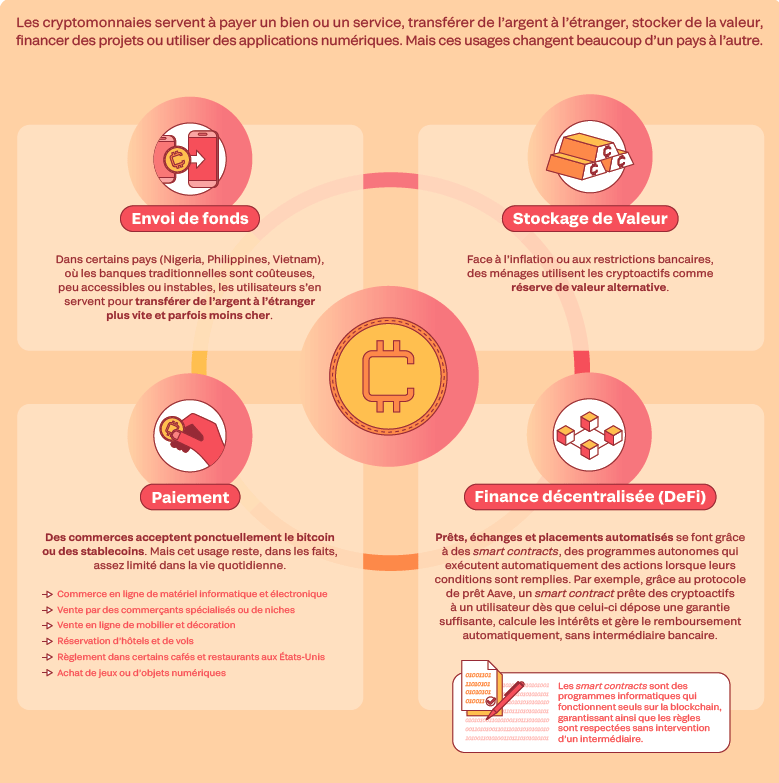

What is it used for?

An economy tested at full scale

For more than fifteen years, cryptocurrencies have operated as a large-scale economic laboratory. Researchers at the Massachusetts Institute of Technology (MIT) have been studying blockchain technologies to understand how strangers can establish trust without banks or other intermediaries and examining how transaction costs can be reduced or redistributed and how rules embedded in code might replace traditional institutional arrangements.

In Europe, the Cambridge Centre for Alternative Finance is studying blockchain systems, examining transaction validation, the role of network participants, energy consumption and the economics of mining, and demonstrating how a monetary system can operate without a central bank, relying instead on shared and collectively verified rules.

Cryptocurrencies are also an ideal testing ground for analysing 24-hour global markets. Bitcoin's price, for example, is a real-time barometer, swinging instantly on economic news, global tensions or exchange collapses. These market reactions give researchers insight into price formation, extreme volatility and collective behaviour.

Finally, crypto-assets also provide a window into regulatory frameworks in the making. The European Union has introduced the Markets in Crypto-Assets (MiCA) Regulation to oversee the issuance and trading of crypto-assets, while in the United States, the U.S. Securities and Exchange Commission is gradually defining where traditional financial assets end and digital ones begin.

Varying adoption from country to country

How are cryptocurrencies used globally? In nations such as Nigeria and India, they facilitate cross-border payments, allowing users to avoid high banking fees. In established markets like the US and Europe, they are mainly tools for investment and portfolio management. The experience of El Salvador, which made Bitcoin legal tender before restricting its use, highlights the challenges of nationwide adoption at scale. The US, Japan and Switzerland recognise Bitcoin as a legal and tradable asset, though not as an official currency. No eurozone country recognises Bitcoin as legal tender.

A substantial energy footprint

Bitcoin uses as much electricity as a country like Poland or Argentina. Proof-of-work blockchains, such as Bitcoin, are the most energy-hungry, as they depend on mining that requires powerful computing resources. Proof-of-stake technologies, by contrast, use far less energy because they avoid the need for intensive computations. Ethereum has operated this way since its 2022 upgrade, known as The Merge, demonstrating how the environmental footprint of crypto-assets is largely determined by the network’s chosen consensus mechanism.

Sociology of crypto enthusiasts

Different movements have emerged within the cryptocurrency space. HODLers (“long-term investors”), for example, advocate for a Bitcoin independent of states, while Ethereum enthusiasts focus on building decentralised applications and emphasise the tangible applications of Web3. Memes, influencers and forums on social media drive both hype and panic. US surveys by the Pew Research Centre in 2024 indicate that crypto owners tend to be young (18–29), predominantly male and generally have medium to high levels of education and income, even though adoption is also significant in some low-income nations.

Institutional turning point

Cryptocurrencies are held by a wide array of actors, including individuals using them for savings and transfers, alongside listed companies and financial institutions. As these new uses emerge, governments are moving to regulate the crypto ecosystem.

Responding to the growing crypto market, the European Union enacted the Markets in Crypto-Assets (MiCA) Regulation in 2023. By protecting consumers, raising transparency standards and regulating stablecoin issuers, Europe has set itself apart as one of the world’s most advanced regulators.

The European Central Bank (ECB), however, has excluded Bitcoin and other cryptocurrencies from eurozone central bank reserves, citing their failure to meet the necessary standards of liquidity, security and stability for sovereign assets. Meanwhile, some central banks are developing official central bank digital currencies (CBDCs), which leverage blockchain-style technology while remaining fully under public authority.

Anti-money laundering authorities are stepping up scrutiny of exchange platforms, given the pseudonymous nature of crypto transactions. In 2023, the UK tightened regulations on misleading advertising, while Japan — following several high-profile cyberattacks — now enforces strict security standards for trading platforms.

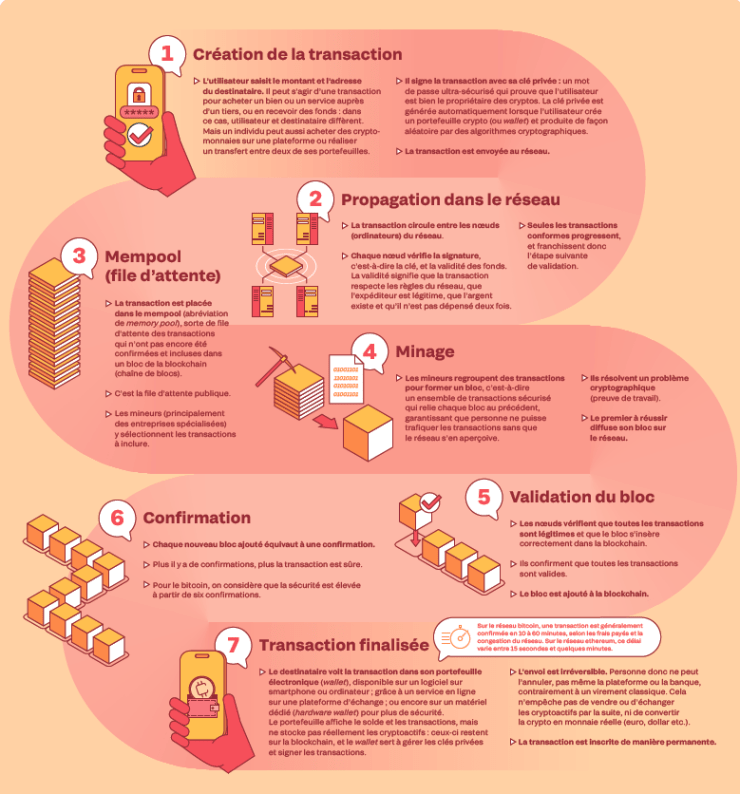

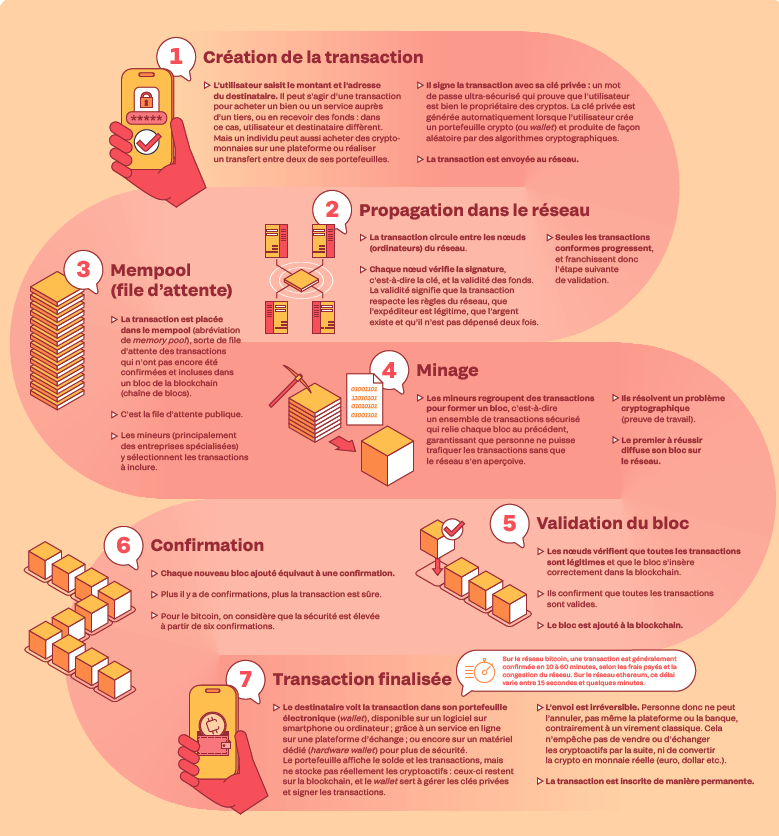

The transaction cycle

A high-risk investment

The primary weakness of cryptocurrencies is their volatility. Between October 2025 and February 2026, Bitcoin lost almost half of its market value, while the collapse of the supposedly “stable” UST stablecoin in 2022 almost wiped out the UST-linked Luna token in just days.

Even with a robust blockchain, users remain vulnerable to cyberattacks, as the surrounding services can contain serious flaws: in 2022, the Ronin blockchain, which powers transactions for the game Axie Infinity, was the target of a theft worth more than $600 million in 2022.

Centralised exchanges like Binance and Coinbase simplify crypto-asset management but introduce risks such as bankruptcy or withdrawal freezes. FTX’s 2022 downfall serves as a cautionary tale: when users rushed to withdraw assets amid solvency doubts, the resulting liquidity crisis forced a halt on transactions. It is a stark reminder that intermediaries create vulnerabilities in a universe intended to bypass them.

Lastly, despite blockchain’s inherent security, scams remain widespread. These include fake projects and “pump and dump” schemes where fraudsters hype a token to inflate its price, only to sell off their holdings at the peak, causing the price to crash and investors to incur heavy losses. A striking example is OneCoin, a fraudulent cryptocurrency that defrauded three million people worldwide of several billion dollars between 2014 and 2017, highlighting the sheer scale of the risk.

Beware: risk of falling!

In 2025, the Bybit platform was the target of a major hack, resulting in the theft of roughly 400,000 Ethereum, with losses estimated at $1.5 billion. The market remains highly volatile, and the withdrawal of a single major actor or widespread panic can lead to dramatic losses within hours. Numerous projects and platforms have failed or been revealed as fraudulent, and some stablecoins or supposedly “safe” financial products have collapsed, wiping out individual savings. Regulatory coverage remains inconsistent, meaning user protections fall short of those provided by conventional banks.

Three possible future outcomes

Even after fifteen years, the global role of cryptocurrencies is far from settled, and economists agree that their prospects remain open to a wide range of possibilities.

One likely scenario, according to financial analysts and institutional actors, is the gradual integration of cryptocurrencies. Banks and financial institutions will continue to explore asset tokenisation, converting real-world assets, such as property, artworks and receivables, into digital assets, as governments pilot the use of stablecoins and blockchain for payment systems and international transfers, and people use cryptocurrencies to send money overseas or to access services online.

In an alternative scenario, cryptocurrencies could remain a specialised niche, used mainly for technical purposes such as DeFi, digital infrastructure and occasional payment applications. For the general public, they would continue to be seen primarily as speculative instruments, highly susceptible to cycles of euphoria and panic.

In a third scenario, cryptocurrencies could undergo a profound transformation. Goods, legal rights and services would be converted into digital tokens, making them easier to trade, while certain paperwork and payments could be automated online. These innovations might give rise to entirely new applications that are difficult to envision today.

The future of cryptocurrencies — whether through integration, specialisation or transformation — will hinge on technological and regulatory developments, widespread public adoption and the practical demands of the global economy.

Glossary

Blockchain

A technology for storing and transmitting data in a secure, cryptographically linked chain of blocks. It operates as a shared digital ledger distributed across many computers, with no central authority, where data is recorded transparently, verifiably and in a way that is difficult to alter. The technology underlies cryptocurrencies, but it also enables a wide range of other applications, such as smart contracts, traceability and certification.

Crypto-asset

A blockchain-based digital asset serving three primary functions: as a medium of exchange, a vehicle for investment and a "key" to access services. All cryptocurrencies are crypto-assets, but not all crypto-assets are cryptocurrencies. Many crypto-assets are primarily used to access or represent something, rather than as a means of payment, such as tokens granting access to an online game or digital platform, or NFTs.

Cryptocurrency

A digital currency used to make payments or transfer value without a bank, such as Bitcoin. Is it a real currency? No. According to national and European central banks, governments, and international bodies such as the G20 and the IMF, cryptocurrencies are not issued by public authorities, do not constitute legal tender and provide no guarantee of price stability. For this reason, these institutions prefer the term “crypto-assets”

Miners

Nodes or participants who contribute computing power to secure the blockchain. Early mining was often done by individuals at home. Today, most mining is carried out by specialised companies operating “mining farms” with thousands of machines, often located in regions with abundant or inexpensive electricity, such as the United States, Canada or Iceland.

Mining

The process by which 'miners' use their computers' processing power to verify transactions and secure a proof-of-work blockchain, such as Bitcoin. Miners earn new bitcoins and transaction fees in return. Mining serves as the network’s guardian, replacing a central authority by ensuring transactions are legitimate.

NFT (non-fungible token)

A unique digital token used to prove ownership of a digital asset, such as an image, artwork or in-game item.

Proof of Stake – PoS

A technological alternative to Proof of Work that replaces computational power with crypto-asset staking as collateral. Participants — validators, not miners — lock up some of their own cryptocurrency. The algorithm then randomly selects validators to validate transactions. Ethereum switched to proof of stake in 2022. This reduced energy consumption by 99% while maintaining a secure network.

Proof of Work – PoW

System used to verify the accuracy of transactions based on computational power. Computers instructed by miners compete to solve complex mathematical puzzles. The first to solve the puzzle validates a block of transactions and is rewarded with cryptocurrency. Bitcoin uses proof of work. The system is considered highly secure but energy-intensive.

Stablecoin

A crypto-asset engineered for stability, with its value pegged to a standard currency like the US dollar or euro. Tether’s USDT is the most widely used and recognised stablecoin.

Token

A blockchain-based digital unit. A token can be used to make payments, access a service, fund a project or represent an asset.